Market Outlook: Last week, there was pressure on the Indian stock market. The benchmark index broke 1.8% to close to the low of August after the US government imposed additional tariffs on Indian goods. Amidst the tremendous selling of FII, even the big purchases of DII could not handle the market. However, there was a slight relief from a potential reduction in GST rate, better monsoon and expectation of fed rate deduction in September.

The market will react to the development related to GDP data better than expected in the first quarter on Monday and the 4 -day visit of Prime Minister Narendra Modi (29 August -1) to Japan and China. According to experts, the week starting from 1 September is likely to remain in a limited range. During this time, the GST Council meeting, auto sales, US job data, manufacturing and services PMI number and Indo-US trade negotiation will be an eye on the market.

Siddharth Khemka, the research head of Motilal Oswal Financial Services, said, ‘We estimate that the market will remain in a limited range. This will focus on strategic meetings with PM Narendra Modi’s top leaders of Japan and China. At the same time, Vinod Nair, research head of Geojit Investments, believes that the market can show a mixed attitude.

Let’s know about those 10 important factor, which will decide the condition and direction of the market next week.

GST Council Meet

At the domestic level, everyone’s eyes will be on the GST Council meeting to be held on September 3-4, in which a final decision will be taken about the slab. This meeting is taking place at a time when an additional 25 percent tariff has been implemented on American goods from 27 August. This has affected sectors like textile, shrimp, footwear, chemical and jewelery.

Most experts believe that the GST reform will be finalized and implemented in September itself, ie before Diwali. Before this, the concessions and tax deduction declared in the budget will strengthen the market’s sentiments and consumption on time.

According to government proposals, soon the 2-per GST system (5 percent and 18 percent) may be applicable. This can include many sectors including fertilizer, textile, footwear, medicines, surgical items, medical devices, education, paper. This information has been given by CNBC-TV18 quoting sources.

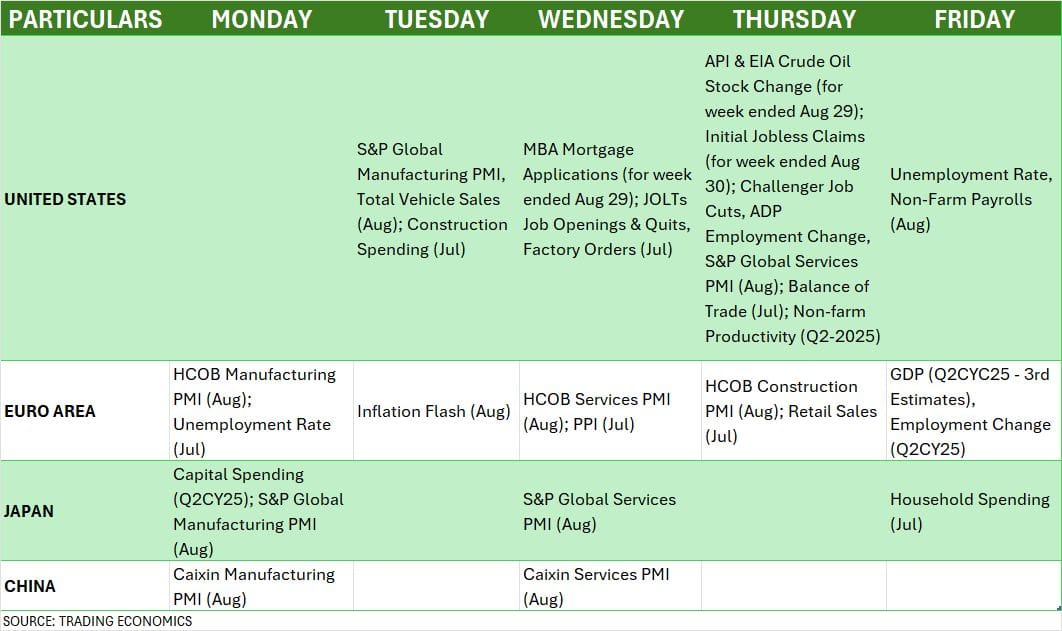

Globally, all the markets will be eyeing the unemployment rate of August and non-form payrolls data after July Jolts Jobs Openings and Quits reports. This will be important in deciding the next policy of Federal Reserve. GDP revision and estimated PCE figures have already indicated the possibility of rate cut in the September policy meeting.

Kaynat Chainwala of Kotak Securities said, ‘Recently Fed Chair Powell has pointed to the risk going down in the labor market. In such a situation, if there is a weakness in the August job report, then the matter of policy eating will be further strengthened.

The final figures of August Manufacturing and Services PMI will be released from major countries like the US, Eurozone, Japan and China next week globally. In addition, August’s flash inflation, July retail sales data and the June quarter of Eurozone will also be in the focus.

Manufacturing and Service PMI

Next week, many important figures on the domestic front will also determine the direction of the market. The final figures of the manufacturing and service PMI of August will be released on 1 September and 3 September. According to initial estimates, HSBC Manufacturing PMI in August reached PMI 59.8 and Service PMI 65.6, better than the final print of July 59.1 and 60.5.

In addition, the details of the week’s foreign exchange reserves ending on August 29 will be released on 5 September. The reserves declined to $ 690.72 billion in the week ended on August 22, while it was $ 695.11 billion earlier.

Focus on auto cells

Automobile sales figures of August will also be declared next week, which will be closely monitored by investors. This can cause a stir in shares of Tata Motors, Mahindra & Mahindra, Ashok Leyland, Bajaj Auto, Hero Motocorp, TVS Motor, Eicher Motors and Escher Motors and Escorts.

FII-DII Activities

The attitude of Foreign Institutional Investors (FII) is currently a matter of concern for the market. He made aggressive selling last week due to change in tariff policies and high valuation. Last week, FII sold shares worth Rs 21,152 crore, causing the total selling of August to reach Rs 46,903 crore. It was Rs 47,667 crore in July. However, he maintained shopping in the primary market.

On the other hand, Domestic Institutional Investors (DII) continuously supported the market and purchased at every decline. He made a purchase of Rs 28,645 crore last week and Rs 94,829 crore in August, which is the biggest monthly net shopping since October 2024.

Rupee at record low

Meanwhile, the rupee also remains a matter of concern for investors. On Friday, the rupee fell 0.66 percent to close at 88.12 per dollar, which is the lowest level ever. It reached 88.31 in Intrade. Long bullish candles were made on the currency chart and it all showed trading above the moving average, thereby signs of short term pressure.

The Indo-US trade war, the hedging demand of the importers and the FPI outflow have increased the pressure on the rupee. However, it is working for partial relief for exporters. Anindya Banerjee, the head of Kotak Securities and Commodity Research Anindya Banerjee, said, “Rupees are still underwelled compared to their emerging market colleagues. However, in the near period, trade war may cause pressure due to concerns. ‘

IPO market condition

Despite the weak benchmark and broad market trends, the primary market will rise. Next week, eight new public issues will open. Of these, only the ₹ 126 crore IPO of Amaanta Healthcare from the mainboard will open on 1 September. The remaining seven issues will be from the SME segment. These include Rachit Prints, Goel Construction, Optivalue Tek Consulting, Austere Systems, Vigor Plast India, Sharma Metals and Vashishtha Luxury Fashion.

Apart from this, the IPO of Oval Projects Engineering, Sugs Lloyd, Snehaa Organics and Abril Paper Tech will be closed next week. At the same time, Anlon Healthcare and Vikran Engineering will be listed on the mainboard on 3 September, as well as 11 listings will be seen in the SME segment.

Technical attitude

Technical charts are indicating that Nifty 50 is currently weak. On Friday, the index took trendline support on the closing basis but it remained below the short -term moving average. The pattern like ‘Shooting Star’, made last week, is indicating Barech Reversal. The negative crossover in MACD and RSI’s lasting at 49.7 is showing weakness. If the index goes below 24,400, then a low test of August may be. At the same time, it is possible to move up to 25,000 on crossing 24,700 upwards.

Nifty Outlook: How will the Nifty move on 1 September, which levels will be experts; Know the expert

F & O Trends and Voltyness Index

Options data shows that there is strong resistance for Nifty at 24,500-24,600. A rally is possible only after standing on top of it. The support is visible at 24,400-24,300 and then directly at 24,000. India Vix rose 0.21 percent to 11.75 this week. Due to low volatility, there is a risk of fast move in the market in any direction.

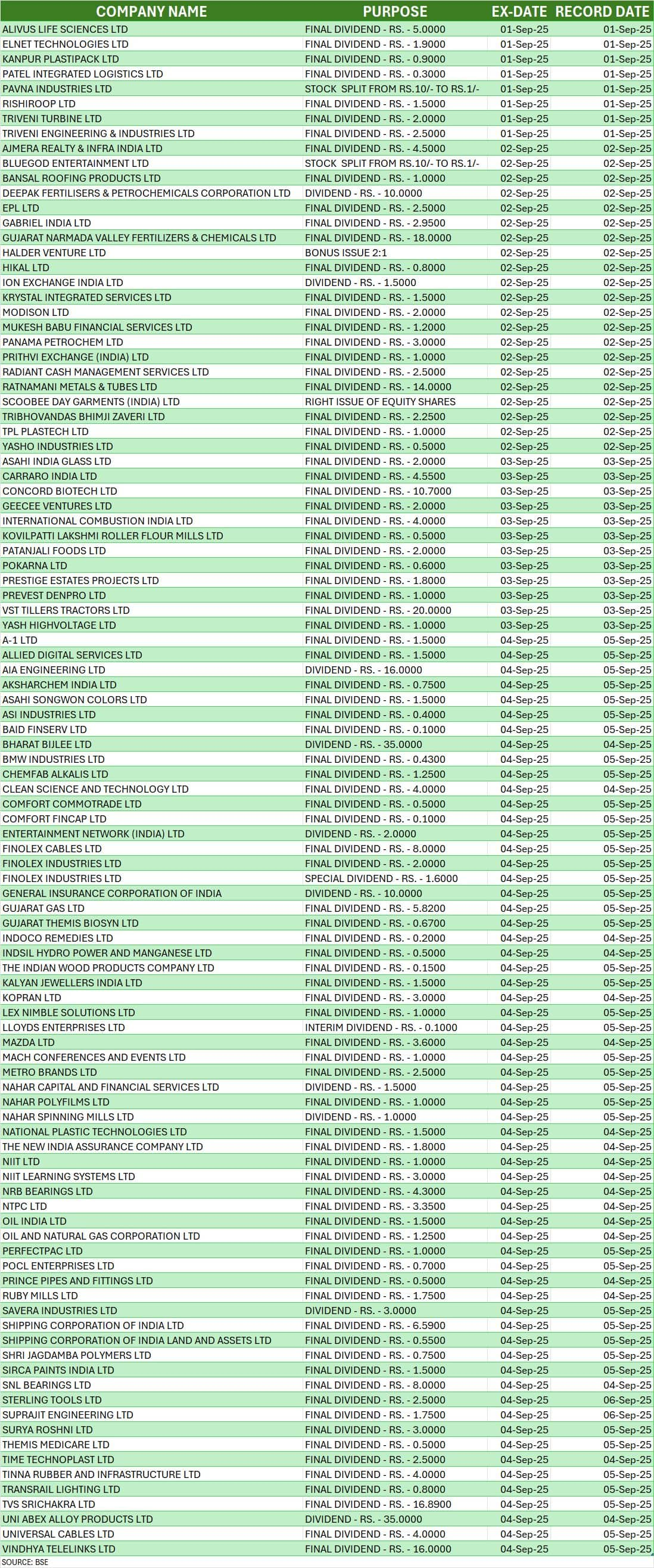

Corporate action

Next week, many companies are also fixed at corporate action like dividend and bonus shares, which will be monitored by investors. (See chart)

Disclaimer: Advice or idea experts/brokerage firms given on Moneycontrol.com have their own personal views. The website or management is not responsible for this. Moneycontrol advises to users that always seek the advice of certified experts before taking any investment decision.